The CPF Board Says Nominations Bypass the Will. The Bank Froze the Account Anyway. Great Eastern Won't Pay the $70,000 DPS Unless You File First. HDB Says Your Mother Can't Keep the Flat Because She Doesn't Meet the Eligibility Rules. And Nobody Told You That CPFIS Investments Require a Completely Separate Probate Application.

Someone in your family has died in Singapore. Within 48 hours you discover that the CPF money everyone assumed would "just come" requires a nomination check — and if no nomination exists, the entire balance goes to the Public Trustee, where it sits for weeks while they charge statutory fees to distribute it under the Intestate Succession Act. The Dependants' Protection Scheme could pay out up to $70,000 in term-life insurance, but Great Eastern will not trigger the claim automatically. You have to find the right form, attach the right medical documents, and initiate it yourself. Nobody calls you. Nobody emails. The money just sits there until you do.

Meanwhile, the bank has frozen every account held solely in the deceased's name. You cannot access the funds to pay for the funeral, the final hospital bill, or next month's mortgage. DBS tells you the joint account is technically still active — but they've blocked deposits, withdrawals, and GIRO until you visit a branch with physical documents they haven't clearly listed. You've heard the Association of Banks is introducing a $5,000 low-balance release, but your branch manager doesn't seem to know the details. The Home Protection Scheme should pay off the outstanding HDB loan, but the CPF Board is still "assessing eligibility" and nobody can tell you when the mortgage will actually be settled.

You searched the MyLegacy portal. It covered the death certificate and pointed you to the CPF Board. The CPF Board website explains nomination rules but does not tell you what to do if the nomination is missing. The HDB website explains Joint Tenancy versus Tenancy-in-Common but does not tell you what happens when the surviving heir doesn't meet HDB citizenship or family nucleus requirements. IRAS wants a final tax return but does not tell you that distributing assets before clearing the deceased's liabilities makes you personally liable. Each agency gives you one piece. None of them gives you the sequence.

The Singapore Survivor Benefits Navigator is a complete Benefits Extraction System built for the reality of Singapore's post-death administration — where CPF, DPS, HPS, WICA, bank accounts, HDB, IRAS, and the Family Justice Courts each hold one piece of your family's financial recovery, and the order you contact them determines whether you receive everything you're owed in three months or lose thousands to fees, missed deadlines, and rejected applications.

What's Inside the Benefits Extraction System

CPF Extraction Guide — Nominated, Non-Nominated, and CPFIS

CPF savings do not form part of the deceased's legal estate. They cannot be distributed via a Grant of Probate. If the deceased made a valid CPF nomination, the funds go directly to the nominees in cash — bypassing probate entirely. If no nomination exists, or if it was automatically revoked by marriage, the money goes to the Public Trustee for distribution under the Intestate Succession Act, incurring statutory administration fees of up to 6.5% on the first $5,000.

But CPFIS investments are different. Funds in the CPF Investment Scheme — unit trusts, shares, gold — are not covered by a CPF nomination. They form part of the legal estate and must be claimed through probate. The Navigator maps all three scenarios (nominated, non-nominated, and CPFIS) with the exact forms, portal steps, and processing timelines so you don't miss money that's sitting in an investment account nobody checked.

Insurance Claims — DPS, HPS, and WICA

The Dependants' Protection Scheme provides up to $70,000 in term-life coverage for CPF members under 65. It is administered solely by Great Eastern Life. The payout is not triggered automatically — you must initiate the claim, submit the death certificate, and provide medical documentation. Processing takes approximately 7 working days once documents are received. The Navigator gives you the exact claim form reference, the submission channel, and the documentation checklist so you can file within the first week instead of discovering this benefit three months later.

The Home Protection Scheme pays off the outstanding HDB housing loan upon death. The CPF Board assesses eligibility automatically after ICA notifies them, but the family is left in limbo on mortgage status. The Navigator explains exactly what happens during the assessment period and when the HDB will finalize the accounting.

If the death occurred during employment, the Work Injury Compensation Act entitles dependants to a statutory lump sum of $76,000 to $225,000. The Navigator walks you through the MOM portal interaction, the employer's WICA insurer process, and the documentation the Ministry of Manpower requires.

Bank Account Unfreezing — Scripts, Rules, and the $5,000 Release

When a bank is formally notified of a death, sole-name accounts are frozen until a Grant of Probate or Letters of Administration is produced. Joint accounts operate under the Right of Survivorship — the surviving holder theoretically inherits the balance — but individual banks impose proprietary restrictions. DBS blocks deposits, withdrawals, and GIRO on joint accounts until the surviving holder visits a branch with physical instructions.

The Navigator provides exact, bank-specific scripts for approaching branch managers, explains the MAS regulatory position on joint accounts, and details the ABS low-balance release protocol (up to $5,000 across accounts without probate) so you can access essential funds during the weeks or months before a Grant is issued.

HDB Inheritance Flowchart — Joint Tenancy, Tenancy-in-Common, and Eligibility Traps

If the flat was held under Joint Tenancy, the deceased's share passes automatically to the surviving co-owner via the Right of Survivorship — overriding the will and intestacy law. But the transfer is not automatic on paper. The surviving owner must lodge a Notice of Death with the Singapore Land Authority, incurring registration fees.

If the flat was held under Tenancy-in-Common or sole ownership, the deceased's share enters the legal estate and must be distributed via probate or the Intestate Succession Act. And even if a beneficiary legally inherits the flat, they cannot keep it unless they independently meet HDB's citizenship, family nucleus, and Minimum Occupation Period criteria. If the inheriting child already owns private property, the HDB may force a sale.

The Navigator includes a visual decision tree that maps your specific situation — tenancy type, citizenship status, existing property ownership, flat purchase date — to the exact outcome and the steps required to execute the transfer or forced sale.

Public Trustee vs. Probate Calculator

For estates under $50,000, the Public Trustee's Office offers a cheaper alternative to private probate. But the PTO operates under strict limitations that create a bureaucratic trap. The PTO cannot administer the estate if the deceased owned unlisted company shares, had a business interest, if beneficiaries are in dispute, if the deceased was the sole lessee of an HDB flat with a child eligible to inherit, or if there are pending lawsuits.

If even one of these conditions exists, the family is rejected by the PTO and forced into the Family Justice Courts — a pivot that delays asset access by 2 to 6 months and incurs unexpected legal fees. The Navigator includes a self-assessment diagnostic that checks every PTO exclusion before you waste time on a rejected application.

Muslim Estates and Faraid Distribution

The Intestate Succession Act does not apply to Muslims. Muslim estates are governed by Faraid under the Administration of Muslim Law Act, administered by the Syariah Court. The interplay between civil law and Syariah law is notoriously complex — joint tenancy properties and nominated CPF monies fall under civil law and bypass Faraid entirely.

Before distribution, specific Faraid deductions must be made: jointly acquired matrimonial property, funeral expenses, and debts to Allah including outstanding Zakat. A Muslim can only will one-third of the estate via Wasiat, and only to non-Faraid beneficiaries. The Navigator outlines the exact dual-court sequence: Syariah Court Inheritance Certificate first, then Family Justice Courts for Letters of Administration.

Tax Clearance and Property Transfer

Executors must settle all outstanding taxes with IRAS before distributing assets to beneficiaries. The Navigator covers Form T filing for trust and estate income, the two-year grace period for maintaining owner-occupier property tax rates after transferring the deceased's property, and the stamp duty implications that catch families off guard when an inherited flat triggers additional buyer's stamp duty on their next purchase.

Repatriation Logistics

For transnational families, exporting or importing remains requires coordination with the NEA, MFA, and Port Health Office. Costs range from $1,150 to over $4,300 for embalming, sealing, and freight. The Navigator provides exact permit requirements — death certificate, embalming certificate, sealing certificate, Coffin Export Permit — and casket dimension regulations for cremation versus burial.

Who This Is For

- Surviving spouses facing frozen bank accounts, uncertain mortgage status, and CPF money they cannot access without knowing whether a nomination exists

- Adult children managing a parent's estate — including those overseas who need to coordinate HDB transfers, IRAS clearance, and insurance claims remotely

- Executors and administrators who need to know the exact filing sequence before they accidentally distribute assets ahead of tax clearance and become personally liable

- Families deciding between the Public Trustee and private probate — especially those who don't know about the PTO's exclusion criteria until they've already waited in the queue

- Muslim families navigating the dual Syariah Court and Family Justice Courts process for Faraid-governed estates

Why Not Just Use Government Websites?

The government websites are accurate. They are also fragmented across at least twelve separate domains — MyLegacy, CPF Board, HDB, IRAS, SLA, MAS, MOH, MOM, the Family Justice Courts, the Syariah Court, the Public Trustee's Office, and Great Eastern (for DPS). Each agency explains its own rules. None of them tells you the order. None of them tells you that checking CPF nominations should happen before you contact the bank. None of them warns you that CPFIS investments require a separate probate application even when the rest of the CPF money goes straight to nominees.

The Navigator does not replace the government websites. It sequences them. It tells you which agency to contact on Day 1, which forms to file in Week 1, which claims to initiate before the 30-day death certificate download window expires, and which applications will be rejected if you haven't completed the prerequisite steps first.

Why Not Hire a Lawyer?

Non-contentious probate fees in Singapore range from $1,500 to $6,500. The Navigator does not replace a lawyer if your estate is contentious or complex. But a significant portion of what probate lawyers bill for is administrative document-gathering — compiling the Schedule of Assets, running the Wills Registry search, gathering bank statements, and preparing court forms. The Navigator walks you through every one of those steps. If you do need a lawyer, you arrive with the documents already compiled, which eliminates the most expensive hours of billable preparation work.

What You Get

- The full Singapore Survivor Benefits Navigator — step-by-step guide covering CPF extraction, insurance claims, bank unfreezing, HDB inheritance, probate preparation, Muslim estate distribution, tax clearance, and repatriation logistics. Updated for 2026 Singapore law.

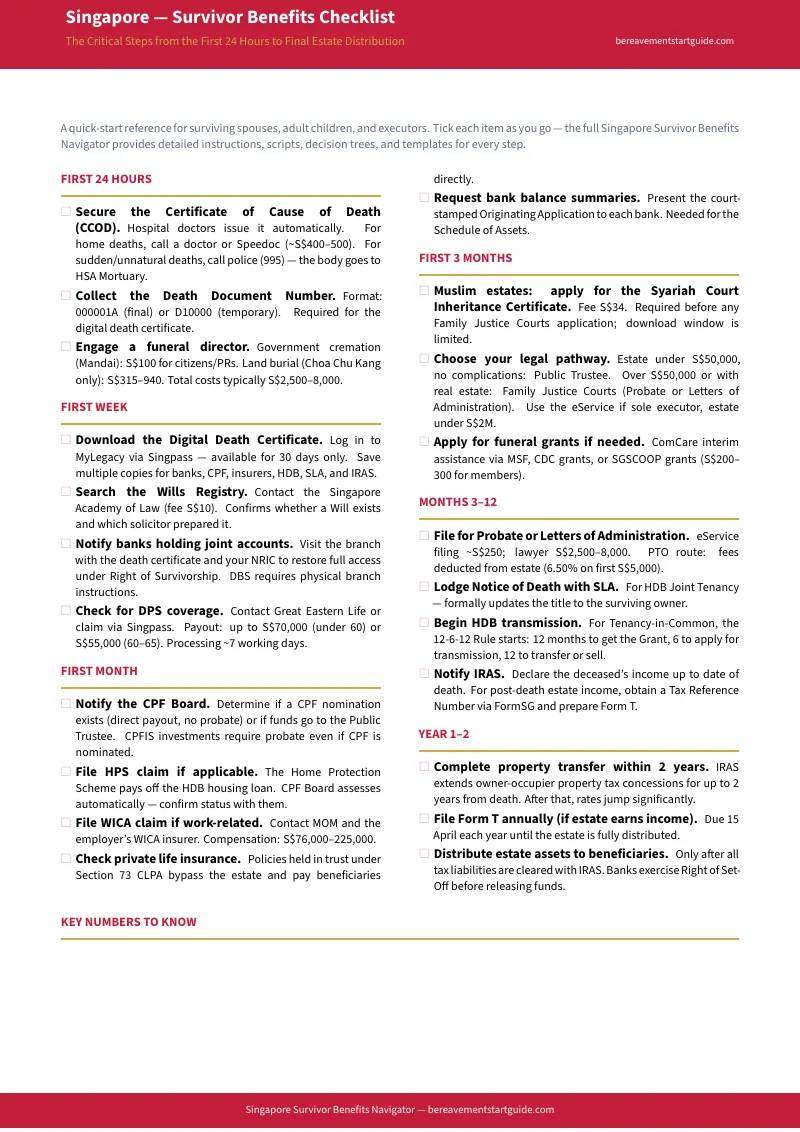

- The Survivor Benefits Checklist — a printable action checklist organised by timeframe (first 24 hours, first week, first month, first three months, months 3–12, years 1–2) so you can track every claim, notification, and deadline without missing a step.

- CPF Extraction Quick Reference — one-page summary of all three CPF scenarios (nominated, un-nominated, CPFIS) with key actions and PTO fee rates

- Bank Unfreezing Scripts — word-for-word scripts to bring to DBS, OCBC, or UOB branch visits, plus the ABS low-balance release protocol and anti-scam hold workaround

- HDB Inheritance Decision Tree — visual flowchart mapping tenancy type, eligibility conditions, and the 12-6-12 Rule to the specific outcome for your family's flat

- PTO vs Probate Diagnostic — one-page self-assessment with all nine PTO exclusion conditions, fee comparison table, and eService eligibility checklist

- Action Timeline — consolidated calendar from the first 24 hours through Year 6+, with every deadline and agency sequenced

- Key Contacts & Portals — quick-reference sheet listing every government agency, portal URL, and what they handle

Satisfaction Guarantee

If you complete the intake checklist and discover your estate requires a lawyer due to complexity, the Navigator will have saved you at least three billable hours of document preparation for your attorney. If you don't find it useful, email us and we'll refund you — no questions.

— Less Than a Single Hour of a Probate Lawyer's Time

Probate lawyers in Singapore bill from $300 to $600 per hour. The Navigator costs . It covers every survivor benefit, every agency notification, every insurance claim, every bank script, every HDB scenario, and every tax clearance requirement — in the order they need to happen. One purchase. One sequence. Every benefit your family is owed.

The free checklist gives you the overview. The full Navigator gives you the forms, the scripts, the decision trees, and the deadlines.