Your Spouse Just Died in South Africa. The Bank Froze Every Account. The Pension Fund Says They Have 12 Months to Decide Who Gets the Death Benefit. The UIF Deadline Is Running. And Nobody — Not the Master's Office, Not the Bank, Not the Government Website — Will Tell You the Full Sequence of Claims You Need to File, in the Order You Need to File Them, Before the Deadlines You Did Not Know Existed Start Expiring.

You are sitting in a Home Affairs queue or standing outside the Master's Office, and the bureaucratic weight of what just happened is starting to hit. The bank called to confirm every account in the deceased's name is frozen — and if you were married in community of property, your joint account went with it. Your debit card was declined at the petrol station this morning. The funeral parlour wants payment. The undertaker handed you a DHA-1663 form and you are terrified of writing a digit wrong in the ID number field, because someone told you an error on this form will cascade through everything — the death certificate, the Master's Office, SARS, the pension fund, UIF, every bank.

Meanwhile, benefits are sitting in five or six different agencies, and not one of those agencies will tell you about the others. The Master's Office handles estate reporting but does not mention UIF dependant benefits. The pension fund is running its own 12-month Section 37C investigation and will not tell you about the GEPF funeral benefit or the COIDA claim. SASSA has unclaimed grant money but nobody at Home Affairs brought it up. The Department of Labour will process your UIF claim but will not mention that you also need the MBU 12 to release funeral funds from frozen bank accounts. Each agency guards its own silo. Your job — in the middle of grief, sleep deprivation, and family pressure — is to somehow discover all of them, file the right forms with each one, and hit deadlines that range from 72 hours to 18 months.

The South Africa Survivor Benefits Navigator is a Claims Sequencing System that maps every survivor benefit available after a death in South Africa, puts them in the order you need to claim them, and tells you the exact forms, agencies, deadlines, and evidence required for each one — so you stop discovering benefits six months too late and start filing them in the right sequence from day one.

What's Inside the Claims Sequencing System

A comprehensive guide and the Survivor Benefits Checklist — covering every benefit source from the moment of death through final pension distribution, built specifically for South African law and the agencies that administer it:

The First 72 Hours: Emergency Cash, Funeral Funding, and the Banking Freeze

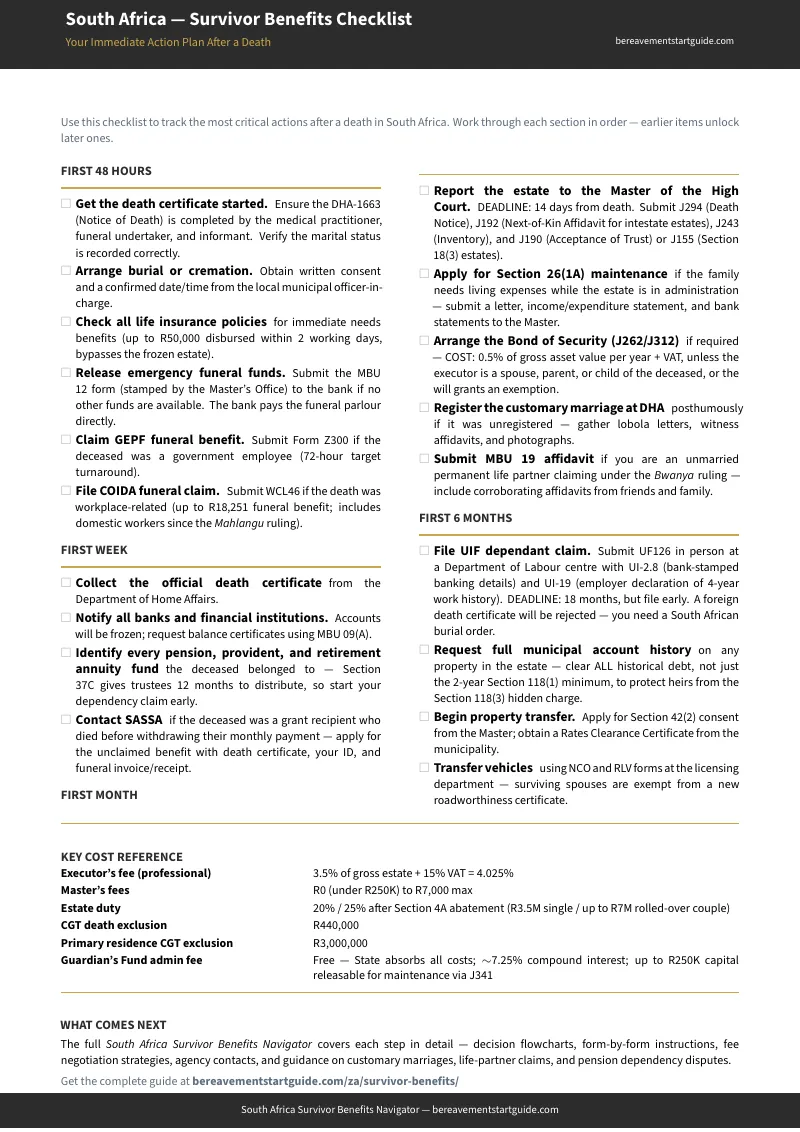

The Administration of Estates Act freezes every bank account the moment the bank is notified — including joint accounts in community of property marriages. This chapter covers the three mechanisms for accessing emergency cash before an executor is even appointed: the MBU 12 form (Master's Consent Letter to release frozen funds directly to the funeral parlour), life insurance immediate needs benefits (up to R50,000 within two working days), and the GEPF Z300 funeral benefit for government employees (target 72-hour turnaround). It also covers the COIDA funeral benefit of up to R18,251 for workplace deaths — including domestic workers, following the Constitutional Court ruling in Mahlangu v Minister of Labour — and how to claim SASSA unclaimed grant payments for deceased pension recipients.

Section 37C: Why Your Will Does Not Control Pension Benefits

This is the chapter that generates the most confusion and the most anxiety. Section 37C of the Pension Funds Act gives the fund's Board of Trustees — not the deceased's will — full discretion over who receives the death benefit. The trustees have up to 12 months to trace every dependant and nominee, investigate financial dependency, and allocate the benefit equitably. During that 12-month blackout, the surviving spouse receives nothing and has no visibility into the process. The guide explains the four allocation scenarios, the difference between a legal dependant and a factual dependant, how to compile an affidavit with bank statements and shared expense records to strengthen your claim, and how to lodge a complaint with the Pension Funds Adjudicator if the final allocation is irrational or unfair.

UIF Dependant Benefits: The Deadline Most Families Miss

When an active UIF contributor dies, the surviving spouse or life partner has 18 months to file a dependant benefit claim using form UF126. Miss the window and the benefit is gone. The guide walks through every requirement: the UI-19 (Declaration by Previous Employers) covering a 4-year work history, the UI-2.8 banking details form that must be signed and stamped by your bank, the in-person submission at a Department of Labour centre, and the surname-mismatch trap that delays claims when your bank records do not match your Home Affairs records. It also covers the claims hierarchy — spouse first, then dependent children under 21 (or 25 if still studying), then nominees — and what happens if a foreign death certificate is submitted instead of a South African burial order.

Customary Marriages, Life Partners, and Bureaucratic Invisibility

The Recognition of Customary Marriages Act says an unregistered customary marriage is still valid. But pension funds, banks, and the Master's Office demand a DHA registration certificate as proof — and if the marriage was never registered, the surviving wife faces bureaucratic invisibility at every institution. The guide covers posthumous registration at Home Affairs, the evidence package required (lobola agreement letters, witness statements from elders, photographs, family affidavits), what to do when the deceased's family refuses to cooperate, and the High Court declaratory order route when Home Affairs declines registration. It also covers the Bwanya v Master of the High Court ruling that gives unmarried permanent life partners inheritance and maintenance rights identical to married spouses — and the MBU 19 affidavit required to establish that claim.

COIDA, SASSA, Property Transfers, Estate Duty, and the Guardian's Fund

The remaining chapters cover every other benefit source: COIDA workplace death benefits (widow's lump sum, monthly pensions for spouse and children, the domestic worker inclusion), SASSA Social Relief of Distress for families in dire need, property and vehicle transfers (Section 42(2) consent, the Section 118(3) municipal debt trap, CRW spouse exemption), the R3.5 million to R7 million estate duty abatement with spousal rollover, capital gains tax death exclusions, executor fee negotiation, and the Guardian's Fund for minor beneficiaries — including how to file a J341 to release funds for school fees, medical bills, and clothing.

Who This Guide Is For

- The surviving spouse whose bank accounts were frozen this morning — who needs the MBU 12 for funeral funds, the Section 26(1A) application for living expenses, and the full sequence of pension, UIF, and state benefit claims mapped out with every form and deadline

- The pension fund dependant waiting for Section 37C — who needs to understand the 12-month investigation timeline, how to compile dependency evidence, and what recourse exists through the Pension Funds Adjudicator if the allocation is unfair

- The customary wife whose marriage was never registered — who is being turned away by institutions demanding a certificate that does not exist, and needs the evidence checklist for posthumous registration or the High Court declaratory order

- The unmarried life partner claiming under Bwanya — who needs the MBU 19 affidavit, supporting evidence requirements, and an understanding of how the Constitutional Court ruling changed inheritance rights for permanent life partners

- The family of a domestic worker or employee killed at work — who needs the COIDA claims process (WCL32, WCL46), the funeral benefit amount, and confirmation that domestic workers are covered following Mahlangu v Minister of Labour

- The adult child coordinating from London, Sydney, or Toronto — who cannot physically visit the Department of Labour or Home Affairs and needs a structured claims roadmap they can work through remotely with a local representative

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across the Master of the High Court website, the Department of Labour portal, the GEPF site, SASSA offices, the Pension Funds Adjudicator's decisions, and a dozen institutional pages that do not reference each other. Here is what you actually encounter when you try to claim survivor benefits using free sources alone:

- Government websites are siloed by agency. The Master's Office explains how to report an estate but does not mention UIF dependant benefits. The Department of Labour explains UIF but does not mention Section 37C pension claims. The GEPF covers its own funeral benefit but says nothing about COIDA or SASSA. Each agency publishes guidance for its own process in isolation. Nobody maps the full sequence of claims across all agencies — which is exactly what you need when you are trying to claim everything you are entitled to within overlapping deadlines.

- Banks and insurers focus exclusively on their own accounts. Standard Bank, FNB, and Absa publish detailed process guides for winding up the deceased's accounts with them. They explain the MBU 12, certificates of balance, and their internal turnaround times. They do not mention UIF, pension fund claims, SASSA, COIDA, or municipal rates rebates. Their guides help you close one account, not claim every benefit.

- Law firm content is lead generation for executor appointments. South African estate attorneys publish thorough articles on customary marriage law, Section 37C, and the Guardian's Fund. Every article ends with a call to action to book a consultation at R1,500 to R3,000 per hour. They have no incentive to explain how a family can compile their own Section 37C evidence package or file a UIF claim without legal representation. Their content is designed to demonstrate complexity, not reduce it.

- Forums give risky anecdotal advice. Reddit's r/PersonalFinanceZA and Facebook diaspora groups are rich with emotional support and real-world stories. But forum advice on intestate succession, pension fund distributions, and tax exemptions is frequently outdated, jurisdiction-confused, or legally wrong. Following a forum recommendation on a Section 37C nomination or a COIDA claim can result in a rejected application that cannot be resubmitted.

Free resources give you fragments from a dozen agencies that do not reference each other. The Claims Sequencing System maps every South African survivor benefit into one document, in the order you need to claim them, with the forms, deadlines, and evidence required for each one.

— Less Than Thirty Minutes With a South African Estate Attorney

A single consultation with a South African estate attorney costs R1,500 to R3,000 per hour. A corporate executor charges 3.5% plus VAT on the gross estate value — R40,250 on a R1 million estate. A missed UIF claim is worth months of dependant benefits that cannot be recovered. A pension fund allocation that goes unchallenged because the family did not know they could file a Pension Funds Adjudicator complaint is permanent. This guide costs less than thirty minutes of professional time and gives you the complete claims sequence — every benefit source, every form, every deadline, and the evidence strategies that nobody charging by the hour will explain to you.

Your download includes the complete guide, the Survivor Benefits Checklist, and 10 standalone reference worksheets you can print individually and bring to the Department of Labour, the Master's Office, the pension fund, or the bank — including the Emergency Cash Toolkit, the Section 37C Evidence Worksheet, the UIF Claims Checklist, the Customary Marriage Evidence Checklist, the Life Partner Claim Worksheet, the Estate Reporting Checklist, the Property Transfer Checklist, the Tax & Costs Reference, the 24-Form Master Reference, and the Master Timeline. Plus a 30-day money-back guarantee. If the guide does not give you clarity on which benefits to claim, in what order, and what forms to bring, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free South Africa — Survivor Benefits Checklist — a structured overview of every benefit source available after a death in South Africa, with the agency responsible, the key form, and the deadline for each one. It is enough to see the full landscape and identify which claims apply to your situation.

You did not cause this crisis. But you can navigate it. The guide shows you how, one claim at a time.